Steel, Still Standing

Post-Safeguard Steel Overcapacity Measures in the European Union and the United Kingdom

The steel safeguards are dead, but steel protection lives on. On 30 June 2026, the safeguard measures that have protected European and British steel industries for eight years reach their legal limit. Both jurisdictions unveiled new instruments designed to tackle global steel overcapacity while sidestepping the constraints that apply to safeguards. Similar objective, different architecture. This briefing examines how the EU and UK have reinvented steel protection as from 1 July and what their new approaches reveal about the evolution of trade defence policy.

Background

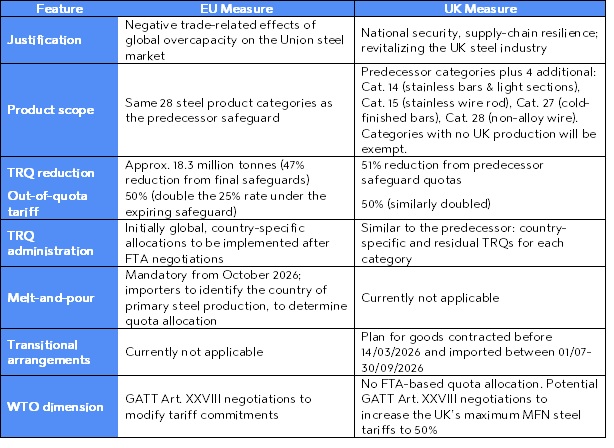

On 1 July 2026, both the European Union (EU) and the United Kingdom (UK) will replace their expiring steel safeguard regimes with new instruments aimed at addressing global steel overcapacity. While widely perceived as successors to expiring safeguard regimes, each is presented as legally distinct and independent from it: the EU measure is a standalone regulation targeting the “negative trade-related effects” of global steel overcapacity on the Union market; the UK measure is a customs tool, presented as a core part of the UK Government’s wider steel strategy.

EU and UK steel safeguards have been in place since 2018 in response to US Section 232 tariffs, which diverted steel exports towards other markets, necessitating tariff quota-based protection under the WTO Agreement on Safeguards (SGA). Following Brexit, the UK replicated much of the EU regime domestically. Both measures were subject to WTO rules requiring, inter alia, progressive liberalisation, exempting developing countries and an eight-year maximum duration. With that ceiling reached on 30 June 2026, neither jurisdiction could legally extend the existing safeguard, and each had to design new instruments outside the WTO safeguard framework.

Design & Legal Structure of the EU and UK Measures

Both jurisdictions framed the underlying problem as global overcapacity and trade diversion. The EU measure, adopted by Regulation (EU) 2026/1384 on 24 June 2026 under common commercial policy, deliberately focuses on negative trade-related effects of overcapacity on the Union steel market. Legal constraints and evidentiary thresholds associated to safeguards are not relevant. The UK measure, on the other hand, is presented as a domestic policy response to strengthen national security and supply chain resilience; but in reality, it largely aims at preventing trade diversion towards the UK following the entry into force of the EU measure. Unlike the former UK safeguard regime (which rested on trade-remedy legislation), the July 2026 regime was announced as a customs/tariff-quota measure, rather than a new statutory instrument.

The overall design of both regimes is similar: (i) both keep the residual + country specific TRQ design from safeguards, (ii) both impose a 50% out-of-quota tariff to categories of steel, and reduce quota volumes substantially; (ii) both are targeting global overcapacity and revitalizing their domestic industries. The principal differences for now lie in matters of scope, legal basis, the EU's melt-and-pour requirement and FTA-based quota allocation.

Exposure to Challenges

Both regimes seek to provide the steel industry with long-term breathing space amid persistent global overcapacity. They are also expected to facilitate structural adjustment and improve competitiveness, which safeguard measures failed to offer. However, despite deliberately distancing themselves from safeguards, potential WTO challenges might arise from the de facto continuity between the old and new systems, given certain structural similarities. WTO panels are not bound by domestic classifications and may assess the measures according to their actual legal and economic effects. Consequently, a panel could conclude that either regime constitutes a continuation of the previous safeguards and cannot be maintained for a period equivalent to the duration of the original measures. Separate grounds may arise on TRQ administration, especially the EU's proposed allocation criteria (e.g., FTA negotiations, compliance with labour and environmental standards, supply-demand). Departure from the requirement that TRQ shares reflect historical trade flows may also attract discrimination claims. The impact of any WTO challenge is nonetheless mitigated by the continued paralysis of the WTO Appellate Body.

Key Takeaways and Future Outlook

Looking ahead, both regimes open to legal challenges, and their WTO consistency will depend largely on the outcome of the ongoing negotiations. In the meantime, the possibility that a WTO panel could characterise either measure as a de facto continuation of the expired safeguards provides exporting countries with a source of negotiating leverage for increased TRQs. Scheduled reviews of both regimes will determine whether the measures evolve into durable long-term solution or require substantial adjustments to catch up with constantly changing market realities.

BLOMSTEIN will closely monitor further developments and keep you informed. If you have any questions, Leonard von Rummel, Uğur Can Hekim, and the entire team is ready to assist you.